- Published by: Tutor City

- January 31, 2024

- Money

How Endowment Plans Can Help You Save For Your Child's Education

Ever found yourself wondering how to secure your child's educational future without breaking into a cold sweat?

As someone who manages a personal finance blog, talked to many of our readers, and worked with financial advisors over the past many years, I've learned a thing or two about planning for education costs.

It's like preparing for a marathon – daunting but doable with the right strategy. And that's where endowment plans come into play.

Did you know that the cost of education is one of the biggest financial burdens for Singaporean families? It's a rising tide that won't wait, and without a solid plan, you could find yourself paddling against the current.

In this post, you'll discover:

- The nuts and bolts of what an endowment plan is

- Three compelling reasons why it's a smart choice for building an education fund

- Key factors to consider when choosing the right endowment plan for your child

I'm here to guide you through this journey, drawing from my personal experiences and professional insights.

So, if you're keen on charting a course towards a financially secure educational path for your little one, you're in the right place.

What is an Endowment Plan?

An endowment plan is a financial product that combines savings, investments, and insurance.

You pay regular premiums over a fixed term, and you receive a lump sum at the end of this term.

This sum includes your savings and, potentially, earnings from the investment component.

Endowment plans are often used for long-term financial goals like funding for your child's education.

3 Reasons to Build an Education Fund With an Endowment Plan

Although there are many ways to build an education fund, let's explore why an endowment plan is often the popular choice to build an education fund for your kids.

#1 Forces you to be disciplined

An endowment plan instils financial discipline.

By committing to regular premium payments, you're essentially setting a structured savings routine.

This approach ensures consistent saving, which might be challenging to maintain with a more flexible saving method.

It's like having a scheduled workout for your finances, ensuring you stay on track towards your goal.

#2 Guaranteed returns

Endowment plans typically offer guaranteed returns, providing a safety net for your investment.

This means a portion of the final payout is assured, often minimally the amount of money you've saved in total, regardless of market fluctuations.

It's like having a safety cushion, ensuring that even in a volatile economic climate, you'll receive a predetermined minimum amount at the end of the policy term.

This feature makes endowment plans a reliable option for long-term financial goals like education funding.

#3 Investment returns

On top of a savings component, the endowment plan invests your money in the insurer's participating funds.

The participating fund is designed to help you grow your money, ensuring that your savings combat the inflation rates.

Remember when chicken rice used to cost $2.50 per plate, but now it can cost up to $4.50?

Well, with an endowment plan, you make sure that the money you save can still pay for the increasing cost of education many years later.

Not only do you save your money, but you grow it, too!

This is where it's important to pay attention to when choosing the best endowment plan, so I'll cover it later.

#4 Tailor it to your specific needs

Endowment plans offer the flexibility to tailor them according to your specific financial goals and circumstances.

You can choose the policy term, premium payment period, and often, the level of coverage.

This customisation allows you to align the plan with your child's educational timeline and your budget, ensuring that the funds are available precisely when needed.

So if you can only save $200/month for the next 20 years, and you need the money 20 years later when your child goes to university, all these can be tailored to exactly how you need it, depending on the flexibility of the endowment plan.

It's like having a bespoke suit – made to fit your exact measurements and preferences.

How To Choose an Endowment Plan for My Child's Education?

#1 Amount you need

Firstly, consider the total amount you'll need for your child's education.

This includes tuition fees, living expenses, and any additional costs.

Calculate the future costs, factoring in inflation, to determine how much you need to save.

This step ensures your endowment plan is adequately sized to meet these future expenses.

Here's a post written by Tutor City as to how much university fees are currently in Singapore.

Compound that with Singapore's average inflation rate of about 2% to 3% over how long you'll be saving, and you'll get a rough amount of how much you'll need to pay for your child's university fees.

This is just a base guideline for you to use, not the education inflation rate. It also doesn’t consider the actual inflation rates and other living expenses your child might need to grow up.

So make sure to consider every expense if you’re trying to calculate roughly how much you’ll need.

#2 Payout age

Next, think about when you'll need the money.

The payout age should align with significant educational milestones, like starting university.

Choose a plan that matures right around the time you'll need to start paying for these expenses, ensuring the funds are available when required.

#3 Capital guaranteed

Next, consider if the plan guarantees your capital.

Capital-guaranteed plans ensure that you get back at least the amount you've put in, regardless of market performance.

This feature is particularly important if you prefer a low-risk approach to saving for your child's education.

#4 Rate of return

The rate of return is crucial as it determines how much your money will grow over the policy term.

Look for plans offering competitive returns by comparing the performance of participating funds of each insurer.

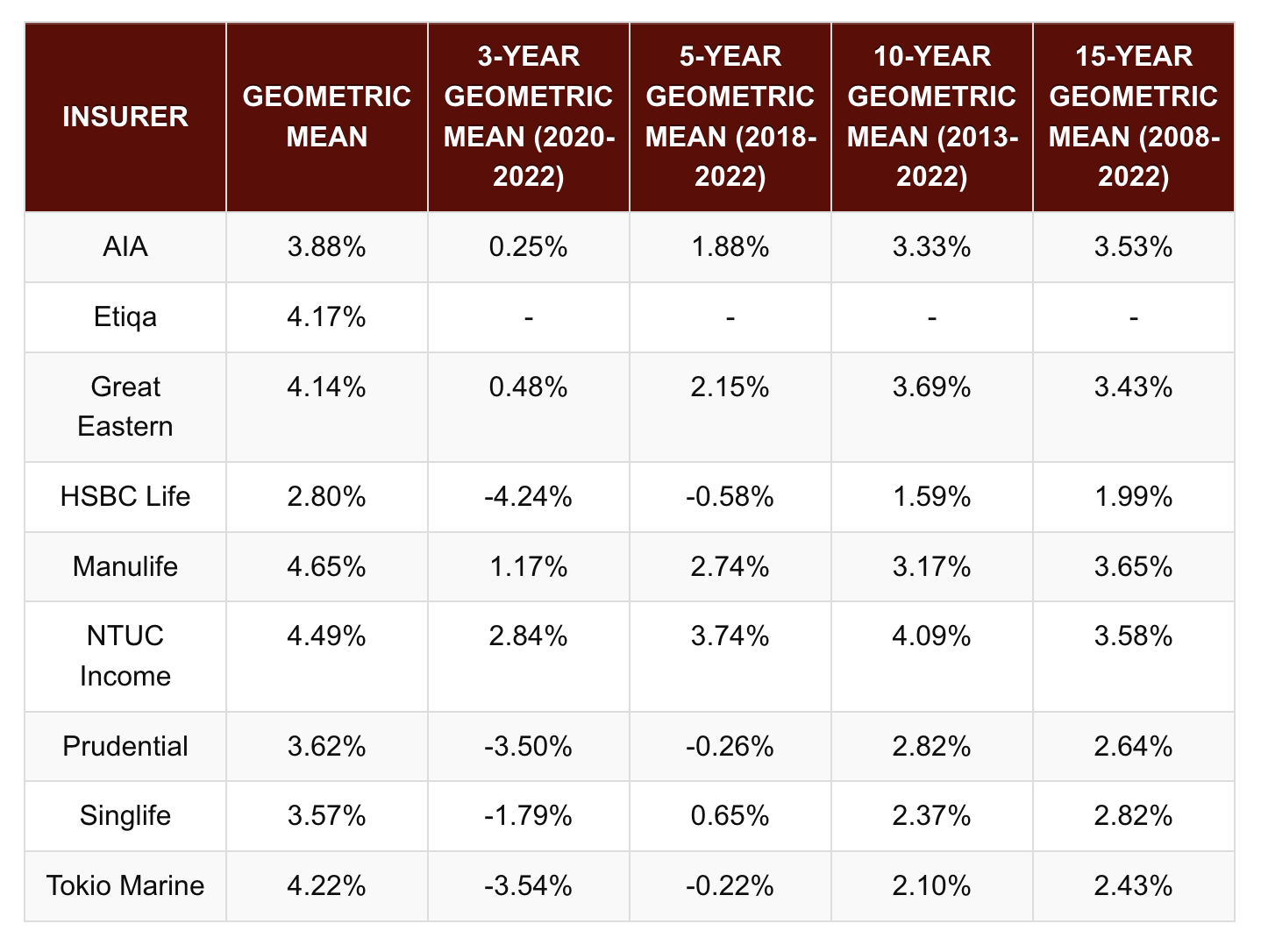

I've compiled the participating fund returns over the past 15 years across major life insurers in Singapore below for you to use as a guideline:

As you can see, Manulife has the highest 15-year annualised returns, while NTUC Income has the highest 10-year annualised returns.

You should compare against when you expect to get the endowment payouts.

So, if it's 15 years later, look at the 15-year performance as a guideline.

Do know that past performance is not an indicator of future performance.

Investment returns aren't the only thing you should consider, as the flexibility of the endowment plan is also important, especially when choosing a policy for your child.

Conclusion

Wrapping up, we've journeyed through the ins and outs of choosing an endowment plan for your child's education.

It's a bit like piecing together a puzzle – finding the right fit for your financial picture.

We've covered the disciplined savings routine an endowment plan enforces, the safety net of guaranteed returns, and the potential for investment growth to keep up with inflation (because let's face it, nobody wants to be caught short when the bill for university rolls in).

We also delved into tailoring a plan to suit your specific needs, ensuring it fits your financial situation like a glove.

And, we've navigated through the crucial steps in selecting the right plan: estimating the amount you need, aligning the payout age with your child's educational milestones, ensuring capital is guaranteed, and scrutinising the rate of return.

Remember, while the past performance of funds like Manulife or NTUC Income can offer some guidance, it's not a crystal ball into the future.

The key is to balance investment returns with the flexibility and security you need.

I hope I've managed to highlight why and how you can use endowment plans for your child's education.

If you enjoyed it, please do share it with your family and friends!

Tutor City's blog focuses on balancing informative and relevant content, never at the expense of providing an enriching read.

We want our readers to expand their horizons by learning more and find meaning to what they learn.

Resident author - Mr Wee Ben Sen, has a wealth of experience in crafting articles to provide valuable insights in the field of private education.

Ben Sen has also been running Tutor City, a leading home tuition agency in Singapore since 2010.